The memory crisis was supposed to be IT’s problem — not Broadcom’s. Broadcom’s VMware pricing changes pushed IT budgets to the breaking point in 2024 and 2025. The financial case for leaving was clear, and organizations across every sector began evaluating alternatives. Then the memory market collapsed, and the cost to exit VMware in many cases exceeded the cost of staying. Broadcom did not engineer this trap, but the memory crisis became its best retention tool.

Key Takeaways

- Broadcom’s per-core subscription model drove VMware cost increases of 300 to 500 percent, making alternatives financially compelling for most organizations.

- AI infrastructure demand hollowed out the server memory and flash supply chain. DDR5 spot pricing increased 6 to 7x in under five months. Enterprise SSD pricing is up 472 percent year over year.

- Server nodes that quoted at $20,000 in January 2026 requoted at $45,000 in late February, with six-month lead times on top.

- The exit math breaks when new hardware costs more than the annual licensing savings the migration was supposed to generate.

- The viable exit path still exists — for organizations whose existing hardware can run an alternative hypervisor without a significant configuration change.

The Licensing Pressure Built the Case

The shift from perpetual VMware licenses to per-core subscription pricing under Broadcom drove cost increases of 300 to 500 percent for most organizations, with some European customers reporting increases above 1,000 percent. An organization that previously paid $50,000 annually now pays $150,000 or more for equivalent coverage. Annual escalation clauses of 5 to 10 percent mean costs compound every renewal cycle. As a result, the financial case for evaluating alternatives became hard to ignore for any organization that ran the numbers.

Key Terms

Per-Core Subscription Pricing

Broadcom’s replacement for VMware perpetual licenses. Organizations pay annually based on the number of CPU cores in use, with no option to own licenses outright. Renewal is mandatory to maintain a supported environment.

Hardware Compatibility List (HCL)

The list of server configurations a hypervisor vendor officially supports. Most alternatives to VMware require hardware on their HCL, which often means newer server generations with current-generation DRAM and storage.

Memory Overhead

The portion of installed server RAM consumed by the hypervisor itself before any virtual machines run. Ranges from 2 to 3 percent in efficient single-code architectures to 15 to 25 percent in layered solutions. At current DDR5 pricing, every percentage point of overhead has a measurable dollar cost.

NAND Flash

The non-volatile storage technology used in enterprise SSDs. NAND and DRAM are manufactured in overlapping semiconductor facilities, which means AI-driven demand for one commodity directly affects supply and pricing for the other.

The Hardware Ambush

Lead Times Make the Math Worse

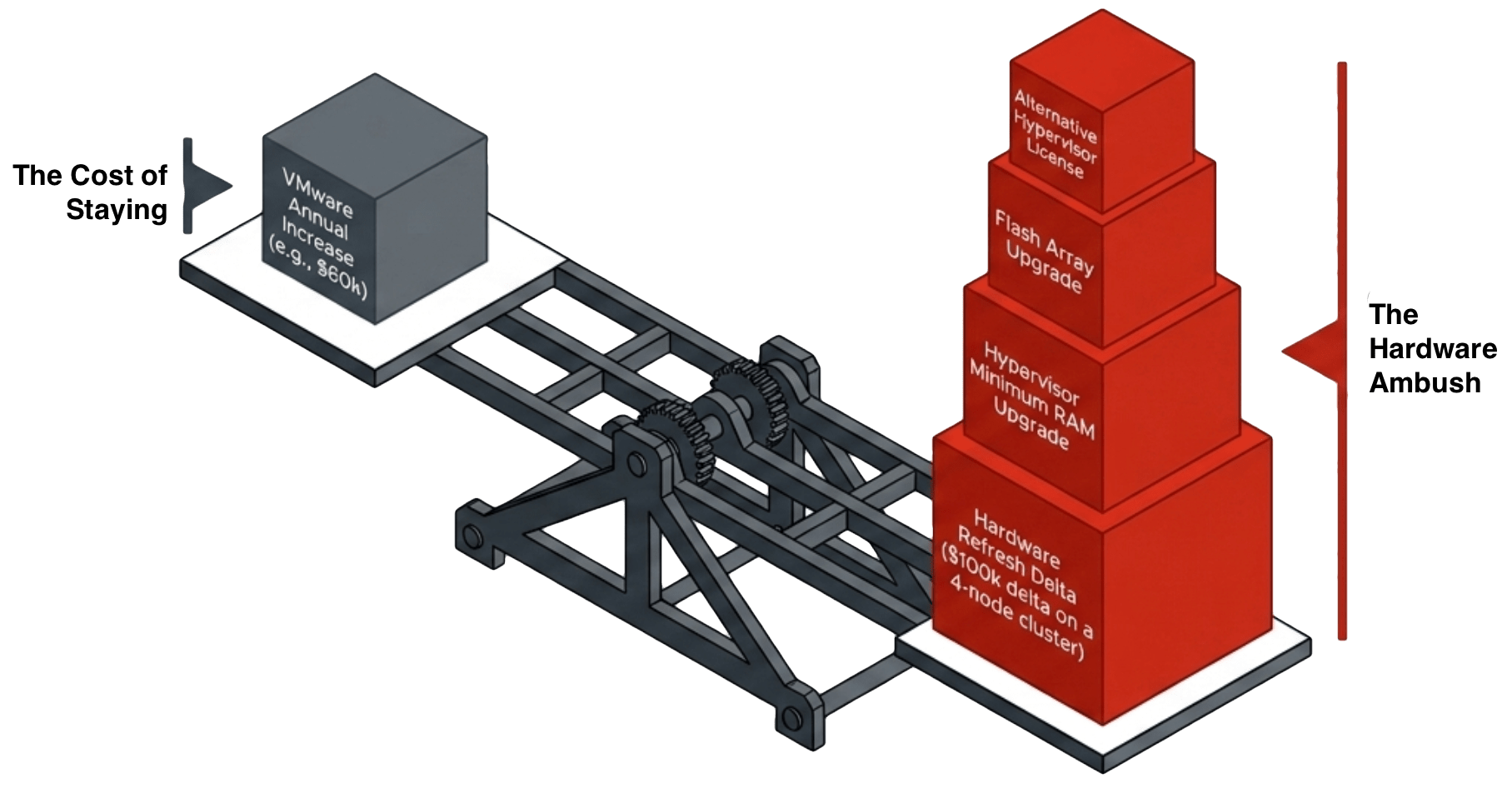

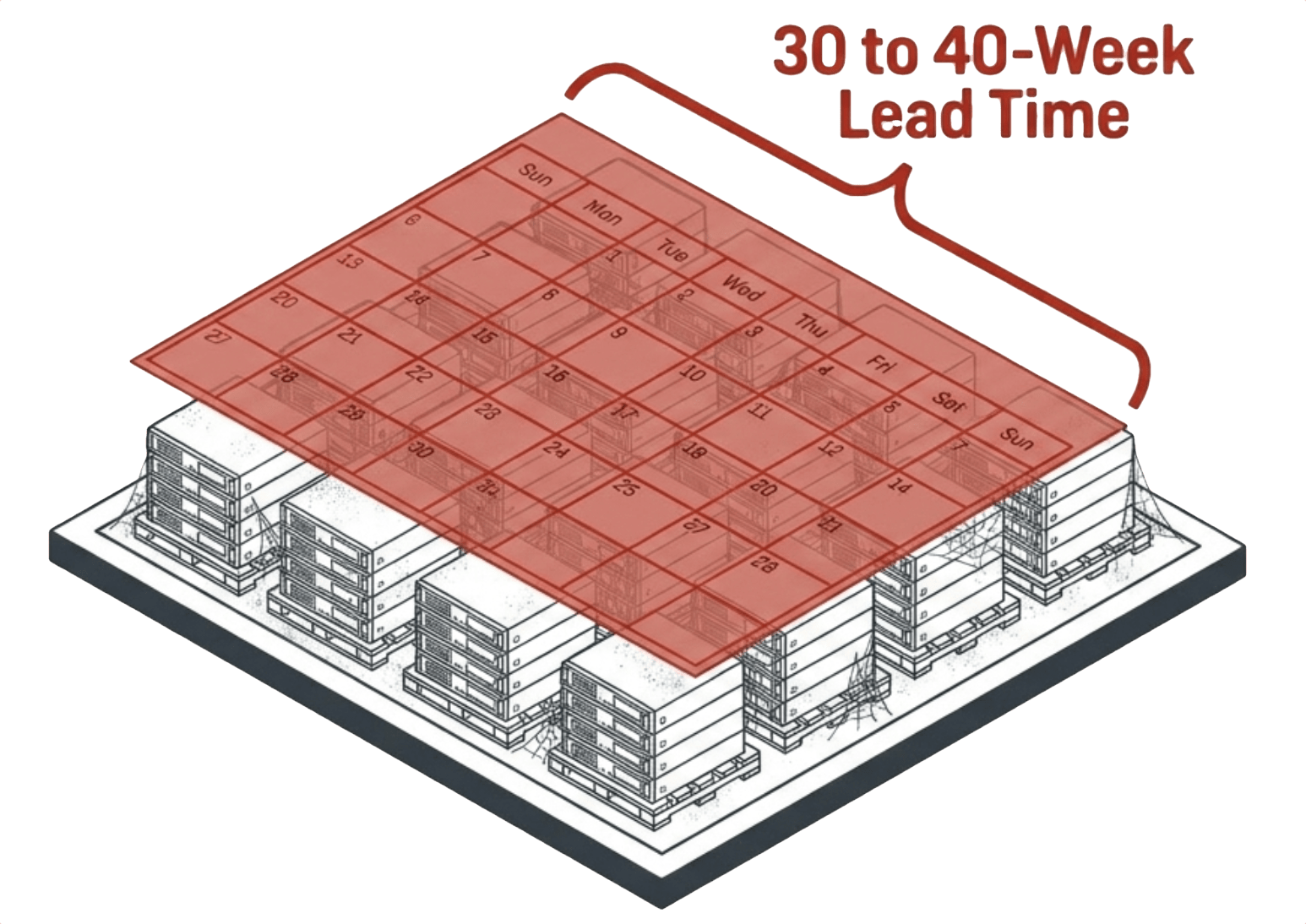

Even if an organization accepts the higher cost and approves the budget, availability is a separate problem. Standard DDR4 and DDR5 server memory is running 30 to 40-week lead times in many configurations. Organizations planning a hypervisor migration in the first half of 2026 may not be able to source the hardware they need until 2027. The exit window has not closed, but the timeline has stretched in ways that change project planning entirely.

Enterprise SSD pricing increased 472 percent between Q2 2025 and Q1 2026. A storage configuration well within budget a year ago now demands a re-approval and often a full redesign. Organizations that planned to refresh flash infrastructure as part of their VMware exit now face a second capital decision stacked on top of the licensing savings they were trying to capture.

How the Memory Crisis Became the Compounding Trap

This is the scenario many organizations now face. VMware licensing costs are rising. The savings from switching are real. The alternative hypervisor is less expensive, and if the right hypervisor is selected, performs well, while clearing the feature parity bar for the workloads that matter. Until IT reviews the minimum hardware requirements or the HCL restrictions.

At that point, IT must get a quote. A four-node cluster refresh from $20,000 per node to $45,000 per node puts the infrastructure delta at $100,000 before any software cost enters the calculation. A memory upgrade to meet the hypervisor’s minimum RAM requirements adds another line. A flash storage upgrade for a dedicated array adds another. If the annual VMware subscription increase is $60,000, the math that justified the exit no longer holds. The organization pays more to leave than to stay for another year.

The deeper problem is that this is not a short-term disruption. Like the housing market, a return to 2023 pricing is not a realistic planning assumption. Building a semiconductor fabrication plant takes approximately five years from groundbreaking to production output. The AI infrastructure buildout consuming memory and flash is not decelerating.

The Exit That Still Works

The exit math does not fail universally. It fails for organizations that need new hardware to make the switch. The organizations that complete successful VMware exits in 2026 will share one characteristic. They will be running alternatives that did not require a hardware refresh. The memory crisis did not close the exit window. It filtered the viable options down to a smaller set.

Some hypervisors have made hardware compatibility their explicit architecture priority. The right alternative checks all three boxes:

- Low memory overhead, broad hardware generation support, and driver compatibility with older configurations mean the hypervisor runs on servers that other alternatives reject outright. An organization that cannot buy new servers today can still complete the migration.

- The ability to aggregate internal consumer-grade or even refurbished SSDs into a cluster-wide virtual SAN removes external all-flash arrays from the bill entirely — eliminating the most supply-constrained and price-inflated component in the migration budget.

- A hypervisor running at 2 to 3 percent RAM overhead versus 15 to 25 percent translates directly to more VM capacity on servers already in production. On a 1TB-RAM server at current DDR5 pricing, that overhead difference is worth more than $20,000 in avoided memory cost per node.

Organizations that find the right hypervisor save in three compounding ways. They exit VMware and eliminate the Broadcom subscription entirely. They avoid a hardware purchase because the right hypervisor runs on the servers already in production. And they get more out of that existing hardware than VMware delivered, because lower memory overhead means more VM capacity per server — effectively extending server life for years and giving the memory market time to settle down and server prices return to something closer to 2023 levels.

VergeOS: Built for This Moment

The storage architecture removes the all-flash array requirement entirely. VergeOS aggregates internal server-based SSDs — including consumer-grade drives and, for organizations willing to manage the risk carefully, refurbished units — into a globally deduplicated cluster-wide storage pool. The deduplication is not a feature toggle. It runs permanently across the entire environment, including cache, network, and RAM, which means a single copy of data in cache is available to every virtual machine in the cluster. In the current market, where a 30TB enterprise SSD costs 22 times the equivalent HDD capacity and external all-flash arrays sit at the back of a months-long supply queue, the ability to avoid that purchase entirely is not a technical preference. It is a budget decision that changes the VMware exit math from a loss to a win.

Frequently Asked Questions

Is the VMware exit still worth pursuing in 2026?

Yes, for the right organizations. The licensing savings are real and the alternatives have improved significantly. The constraint is hardware. Organizations that can run an alternative on their existing infrastructure can capture the savings immediately. Organizations that need new hardware face a cost delta that may exceed the near-term licensing savings, depending on configuration.

Which organizations are most exposed to the hardware trap?

Organizations whose servers are older or use configurations not on a modern HCL, and organizations planning to refresh hardware anyway as part of a migration. The trap is worst for buyers counting on the hardware refresh as a natural part of the exit who have not yet priced the current market.

What should IT teams look for in a VMware alternative given the hardware shortage?

Prioritize hypervisors that support the hardware currently in production, not just the latest generation. Ask specifically: what do I need to change about my existing hardware to run your software? A hypervisor that requires a RAM upgrade or a minimum hardware generation to get deduplication or full feature support has just shifted the cost equation significantly.

How long will the memory crisis last?

New semiconductor fabrication capacity takes approximately five years to bring online. AI-driven demand for memory and flash is not projected to slow. Meaningful price normalization is more likely in 2027 or 2028 than in 2026. IT leaders planning infrastructure refreshes should model current pricing, not 2023 benchmarks.

George Crump is the Chief Marketing Officer at VergeIO, the leader in Ultraconverged Infrastructure. Prior to VergeIO he was Chief Product Strategist at StorONE. Before assuming roles with innovative technology vendors, George spent almost 14 years as the founder and lead analyst at Storage Switzerland. In his spare time, he continues to write blogs on Storage Switzerland to educate IT professionals on all aspects of data center storage. He is the primary contributor to Storage Switzerland and is a heavily sought-after public speaker. With over 30 years of experience designing storage solutions for data centers across the US, he has seen the birth of such technologies as RAID, NAS, SAN, Virtualization, Cloud, and Enterprise Flash. Before founding Storage Switzerland, he was CTO at one of the nation's largest storage integrators, where he was in charge of technology testing, integration, and product selection.

[…] in January 2026 re-quoted at $45,000 in late February — a dynamic also examined in depth in The Memory Crisis is Broadcom’s Best Retention Tool. For organizations planning to migrate away from VMware to capture licensing savings, the hardware […]

[…] have called the memory crisis Broadcom’s best retention tool — and that framing is accurate for organizations that need new hardware to complete the […]